One year after the commencement of World War I the Federal Government legislated its first income tax act alongside the state legislation – the Income Tax Assessment Act 1915.

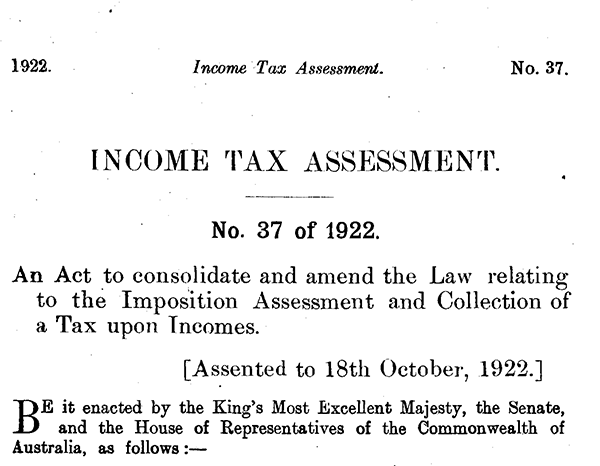

When McCullough Robertson formed in the 1920s, Australians were taxed both by the States and the Commonwealth through the Income Tax Assessment Act 1922 (Cth), which included measures such as:

1. If a company did not distribute at least two-thirds of its taxable income in a year, the Commissioner could require the company to pay additional tax equivalent to the amount that would have been payable in the hands of its shareholders.

2. Every agreement or arrangement that altered income tax, including to relieve liability, defeat, evade or avoid income tax, was absolutely void without prejudice to its validity in any other respect.

Income tax rates in the 1920s

Income tax rates were governed by the Income Tax Act 1926, which for personal exertion started at three pence per pound and increased by three eight-hundredths of a penny per pound, up to the top rate of sixty pence per pound sterling above £7,600. For companies, the rate was one shilling per pound sterling. There were 20 shillings in a pound, and 12 pence in a shilling, so the minimum personal exertion tax rates started at 1.25%, and increased to a maximum 25% for amounts over $750,000 in today’s dollars (adjusted for inflation). Corporate tax rates were a flat 5%. This was in addition to State income tax.

DID YOU KNOW

The 1922 Act, which comprised only one hundred sections, is now replaced by the modern tax legislation: a seven volume Income Tax Assessment Act 1936, twelve volume Income Tax Assessment Act 1997, and four volume Taxation Administration Act 1953.

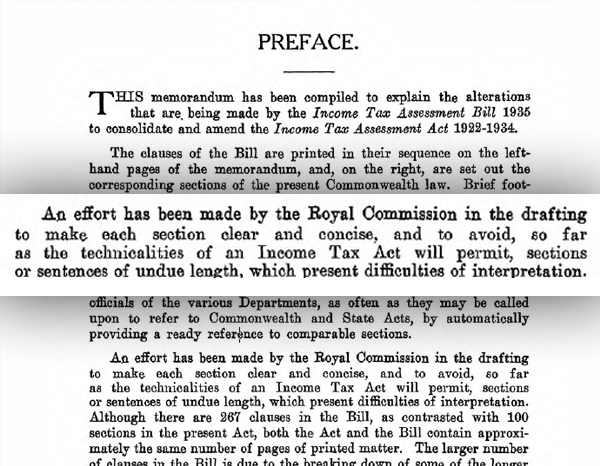

Within six years of the formation of McCullough Robertson, a Royal Commission was appointed to harmonise the Federal and State legislation which resulted in the Income Tax Assessment Act 1936 (Cth) (1936 Act) and, in Queensland, the Income Tax Assessment Act (Qld).

In the 1940s, the Federal Government enacted legislation to increase its revenue from income tax and to effectively end State income tax.

The 1936 Act remains in force today with the original provisions from 1936 still governing Australian tax, including:

· the definition of a tax ‘resident’;

· the provisions on tax anti-avoidance schemes, which were re-drafted in the late 1970s into Part IVA;

· Division 6 on the taxation of trusts, which has had new sections and concepts patchworked in the last 90 years;

· the taxation of private companies’ undistributed income, which moved from taxation of the company to the shareholder in the 1990s.

With the introduction of numerous amendments and new tax acts, the complexity of the 1936 Act exponentially increased and in the 1990s, the Government commenced a project to rewrite the act - The Income Tax Assessment Act 1997.

In 1901, the Customs Act and Excise Act were enacted and replaced separate excise and customs duties levied by, as well as between, the States.

125 years later, we continue to advise clients on state-based legislation which may impose a duty of customs or excise, which is reserved for the Federal Government.

The Customs Act and Excise Act established how the import of goods and manufacture of alcohol, fuel and tobacco (excisable goods) were levied, based on Federal visibility and Government control over the goods until the duty was paid. More than a century on, the Acts remain in force unchanged, and struggles to remain functional in the 21st century.

Australian markets opened in the 1950s following the introduction of sections 60 and 35A of the Excise Act and Customs Act (respectively), which enabled Australians to import or manufacture goods without paying duty upfront or providing security. However, this created a nearly absolute liability for anyone that had possession, custody or control of the goods, which applied short of “Godzilla stomping on the goods” (Drew v Dribb (2008) 169 FCR 320, 326).

We have recently seen the Collector of Customs issue demands, based on legislation from 1901, allegedly for unpaid duty simply because the Collector considered the goods too cheap. Under the Collector’s current arguments about the application of the legislation, anyone from an importer, to a truck driver, to the final consumers could be liable. We discuss the practical implications in our article here.

Senior Associate, Adria Askin’s wish for tax reform is to see the long overdue modernisation of these early 20th century concepts so that the law reflects today’s realities.

When McCullough Robertson was formed, fixed trusts were used in Australia as they were in England: by landowners and wealthy families to manage estates and transfer wealth.

A single section of the Income Tax Assessment Act 1922 (Cth) addressed the taxation of a trustee and beneficiary – today, this has been replaced by Division 6 of the 1936 Act.

Through the 1970s and 80s, trusts also rose to prominence for use by charities, businesses, and as investment structures, and discretionary trusts emerged and became popular for asset protection and tax planning. Unsurprisingly, the increased use of trusts has led to increased regulatory attention.

Section 99B was introduced to tax income that was accumulated in a foreign trust and fell outside the Australian tax net when later distributed to an Australian resident beneficiary.

Section 100A addresses tax avoidance through reimbursement agreements, which is when persons enter into an agreement to make a beneficiary presently entitled to trust income but distribute the income to another person, with the purpose of reducing or eliminating that other person's tax liability, unless the agreement forms part of ‘ordinary family or commercial dealings’.

The ATO has turned its attention to trusts – including more recently, the meaning of the exclusion for ‘ordinary dealings’ and the application of section 99B. Both sections have complex language, and have not been updated in light of significant legislative changes like the introduction of capital gains tax (CGT) and changes in international tax provisions. Difficult to interpret and apply, the ATO issued its view of the sections in TR 2022/4 and PCG 2022/2 regarding section 100A, and PCG 2024/3 regarding section 99B with, at times, limited reference to the law. Learn more about section 100A here.

While the first payroll tax scheme was introduced in New South Wales in 1927, (just after the formation of McCullough Robertson), in 1941, the Federal Government obtained the right to tax wages, with the first federal payroll tax regime introducing a levy of 2.5% on all wages. This was key to funding Australian Federal Government programs during World War II alongside income tax.

In 1971, the Federal Government transferred the right to tax wages back to the states and territories and it became (and remains) a significant source of revenue for the states. All states enacted payroll tax legislation around this time, with the Northern Territory following in 1978, and the Australian Capital Territory in 1987.

From there, each jurisdiction established its own rates, thresholds and rules. As reliance on this revenue grew, Commissioners took an increasingly aggressive approach to the application of grouping provisions and employment agency provisions.

The result? A complex and inconsistent regime that has frequently left clients who believed they were compliant facing unexpected historical assessments, that are both costly and difficult to dispute.

While many recognised the need for harmonisation, meaningful action did not begin until 2008.

In 2008, Queensland, New South Wales, and Victoria moved to harmonise their payroll tax legislation, with other jurisdictions following subject to some minor differences.

The harmonisation of payroll tax following its introduction in 1970 is crucial to the effective operation of the regime. With modern workplaces offering significantly flexibility for where work is performed, the consistent approach across Australian jurisdictions reduces the scope for employers to minimise their payroll tax by locating employees in lower tax jurisdictions.

However, payroll tax continues to create anomalous outcomes and in recent years, we have seen an expansion of the types of arrangements the Offices of State Revenue seek to assess for payroll tax.

Senior Associate, Sammuel Dobbie-Smitham’s wish for tax reform is to see greater legislative or judicial clarity on where payroll tax employment agency provisions will be engaged and how payroll tax is applied to employment agency arrangements.

These issues were explored in Integrated Trolley Management Pty Ltd v Chief Commissioner of State Revenue [2023] NSWSC 557, a key case in the interpretation and application of employment agency provisions which Sam was involved in, prior to joining McR.

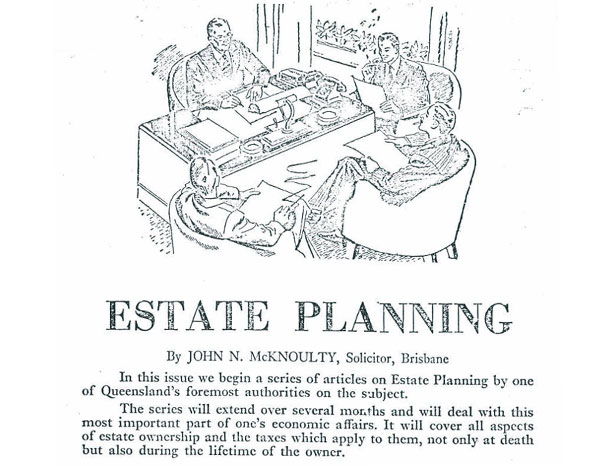

Death duties historically were imposed in Australia on the value of inherited assets and had a significant impact on farming families and other small businesses as there was usually no cash to pay the duties, necessitating a sale of assets in lieu of family succession.

In the 1970s, McR Partner, John McKnoulty, was influential in changing the laws relating to death duties. At the same time, John pioneered the firm’s renowned regional outreach program, travelling throughout the State to meet with landowners and referrers.

DID YOU KNOW

Queensland premier Joh Bjelke-Petersen led the State’s push to abolish death duties in the late 1970s for gifts to spouses, and other states (and the Commonwealth) followed Queensland’s lead over the following years.

Following in his father’s footsteps, Consultant, Peter McKnoulty’s wish for tax reform is to introduce tax and duty concessions to facilitate a more efficient intergenerational transfer of assets.

McCullough Robertson reached its half-century in the 1970s during the infamous ‘bottom of the harbour’ era, during which tax avoidance was rife in Australia.

The key anti-avoidance provision, section 260, remained unchanged since the 1920s, and taxpayers were greatly abetted by the courts taking a strictly literal approach to statutory interpretation. Thus talented tax advisers could concoct schemes which were technically correct and yet did not amount to anti-avoidance.

McR was involved in Tupicoff v Commissioner of Taxation (1984) 4 FCR 505, a case concerning the operation of the old tax avoidance provision to an income splitting arrangement concerning an insurance agent’s use of a discretionary trust. Unlike many such arrangements, Mr Tupicoff was unsuccessful in his appeal.

In 1981, Part IVA was introduced, joining the ATO’s arsenal against tax avoidance arrangements including the new section 100A, section 99B and later, Division 7A.

The ATO’s view on tax avoidance continually changes and has swung back toward overreach, often outside the parameters of legislation. It is particularly frustrating when the ATO publishes its views contemporaneously or not at all.

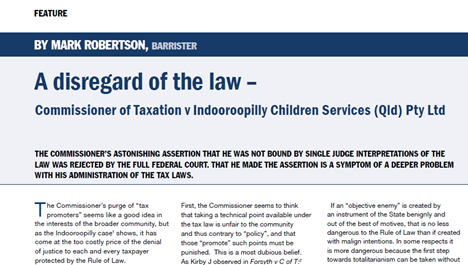

Under the new avoidance regime, McR acted for the taxpayer in Essenbourne Pty Ltd v Commissioner of Taxation (2002) 51 ATR 629 where Kiefel J (as her Honour then was) found for the taxpayer, and held the relevant arrangement did not attract FBT and that Part IVA did not apply. The ATO did not appeal the decision in Essenbourne, which was followed in at least one other decision, and continued to apply its interpretation of the law which was set out in its taxation ruling until it rana case on an identical issue, Commissioner of Taxation v Indooroopilly Children Services (Qld) Pty Ltd (2007)158 FCR 325. The Full Court of the Federal Court of Australia dismissed the ATO’s case with strong criticism of the ATO’s conduct.

This raised questions regarding the Commissioner’s failure to adhere to the rule of law.

The ATO’s view on tax avoidance continually changes, often targeting arrangements arguably outside the original parameters of the legislation.

The ATO’s view on tax avoidance continually changes, often targeting arrangements arguably outside the original parameters of the legislation.

Partner, David Hughes, and Lawyer, Jordi Morgan’s wish for tax reform is for the Commissioner to provide greater certainty to taxpayers by not seeking to alter long-established positions. David says the “The Commission’s approach to statutory interpretation and administration (including audit activity) has not always been transparent and often lacks certainty. On difficult issues (such as unpaid present entitlements, section 100A, and section 99B), the Commissioner’s current approach seems to be to continually seek to evolve and expand the reach of legislation which has been around for fifty years or more. Certainty and consistency are the hallmarks of a fair tax system.”

CGT was introduced in 1985 and fundamentally changed Australia’s tax landscape, bringing transactions that were previously tax free, within the tax net.

CGT complicated restructures, transactions and the passing of generational wealth, with limited relief available through rollovers and concessions.

Rollovers are a key part of most business restructures, although have recently caught the eye of the ATO as being used as part of potential tax avoidance arrangements under Part IVA. The Government has also recently considered expanding CGT to tax unrealised capital gains in proposed superannuation amendments (Division 296).

Advising on CGT implications remains a core part of our work with clients.

Senior Associate, Melissa Simpson’s wish for tax reform is for the interaction and consequences of CGT rollovers and subsequent consolidation to be amended to ensure both can be used to achieve what is clearly intended; for the small business CGT concessions thresholds to be increased in accordance with CPI, and for the CGT regime to never be expanded to taxing unrealised capital gains.

Before 1910, the minerals in the ground were the property of the owner of the land. From 1910, title to all minerals was claimed by the Australian States; anyone extracting those minerals had to pay a royalty to the State.

DID YOU KNOW

Happily, anyone who owns land with a title granted before 1910 continues to keep any royalties from their land (even now!)

In 1989, a uniform royalties regime was introduced under the Mineral Resources Act 1989 (Qld). Before then, there were varying royalty rates which applied and the rate specified under the Central Queensland Coal Associates Agreement was 5 cents per tonne of coal mined. The top rate of coal royalty in Queensland is now 40% ($120 per tonne) for coal valued at more than $300 per tonne (one of the highest mineral royalty rates in the world)! So, the royalty streams are extremely valuable to the State.

The administration of royalties transitioned from the Department of Mines to the Queensland Revenue Office (QRO) in 2011. Since then, the QRO have stepped up audit and compliance work, leading to numerous Court cases.

DID YOU KNOW

In 2024/25, mineral royalties contributed approximately $1.5 billion to Queensland revenue.

The petroleum royalties regime in Queensland was fundamentally overhauled in 2020 from a value model to a volume model. This raises even greater concern as to whether the new regime is a ‘duty of excise’ and therefore outside of Queensland’s constitutional power to impose.

Joint Managing Partner, Damien Clarke's wish for reform is "for a simplified tax regime which applies consistently throughout Australia so as to remove the revenue law barriers to investing in Australian assets and people. The abolition of antiquated State taxes such as payroll tax and stamp duty (even if at the expense of an increase in the GST rate), the reduction in the punitive rates that are charged for Queensland coal royalties and the removal of the duplication of costs caused by having both State and Federal revenue authorities would be a good start."

Superannuation pre-dated the formation of McR, and when Federal income tax was imposed in 1915, superannuation funds were exempt from income tax, and unlimited deductions were available for contributions made on behalf of employees.

As McR reached its pension age in the 1990s, the superannuation guarantee was introduced alongside new industry supervision legislation.

In the decades since, the legislation and the ATO’s interpretation of superannuation obligations has shifted from a focus on Australians contributing and providing for their retirement, to ensuring Australian's access to the tax-concessionary treatment in superannuation funds is restricted.

The McR Tax team successfully assisted a client in non-arm’s length income (NALI) proceedings before the Administrative Appeals Tribunal (as it then was) where the ATO sought to apply notions of commercial and legal perfection to the conduct of our client – BPFN v Commissioner of Taxation [2023] AATA 2330, discussed here.

As McR approached its three-quarter century, the Income Tax Assessment Act 1997 was introduced as part of the Tax Law Improvement Project, a comprehensive effort to overhaul the outdated 1936 Act and replace it with plain English drafting to enhance accessibility and understanding.

The 1997 Act was the first and only instalment of the rewrite of the 1936 Act and partly achieved this purpose however, its complexity reflects the intricate nature of tax legislation.

DID YOU KNOW

The 388-page 1997 Act alone now traverses 12 volumes and must be interpreted alongside the 1936 Act (including a number of repealed provisions) and the Taxation Administration Act 1953.

To help reduce the complexity around income tax, Lawyer, Paige Milton’s wish for tax reform is to complete the planned rewrite of the 1936 Act and consolidate the 1936 Act and the 1997 Act. This would provide a unified and modernised framework which would enhance clarity, reduce compliance costs, and improve accessibility for all taxpayers.

Division 7A was introduced on 4 December 1997 to tax shareholders and their associates on payments, loans, made to them, or debts forgiven debts by, private companies. This concept was first recognised in the context of corporate taxation when McR formed in the 1920s (since replaced), although at that time the company (not shareholder) was taxed on undistributed profits.

Division 7A created significant implications for how private companies and their shareholders and associates interact.

Notwithstanding these rules have now been in place for almost 20 years, we still regularly assist clients and their advisers to navigate the application of Division 7A, including making applications to the ATO for tax relief where there has been a genuine mistake in applying and litigating matters concerning the ATO’s interpretation and application of Division 7A, - which continues to change over time -for example, the treatment of unpaid present entitlements (UPEs) from trusts to companies. The ATO treated UPEs as loans for Division 7A, requiring compliance with commercial and repayment terms for many years and issued a ruling on this basis. In the past two years, the Federal Court and Full Federal Court confirmed that the ATO’s view is incorrect Commissioner of Taxation v Bendel (2025) 307 FCA 544. Read more about the Bendel case here, which is on appeal to the High Court.

The ATO continues to administer arrangements in accordance with its pre-existing views (an approach for which there is precedent) with similar behaviour seen in the context of section 100A and Part IVA.

Special Counsel, Jodie Robinson, and Senior Associate, Elise Emmerson, share a similar wish for tax reform: simplifying Division 7A to encourage compliance and reduce the costs of compliance.

Australia first introduced specific Employee Share Scheme (ESS) rules in 1999 to provide clear tax treatment for shares and rights given to employees in the course of their employment. Still today, share and option incentive schemes are a popular way for employers to reward and incentivise key employees.

The ESS rules were introduced with a view to ensuring that non-cash equity awards provided to company employees are taxed appropriately.

Even with the introduction of certain ‘tax advantaged’ schemes, such as the deferral concession and start up concession, Australia’s ESS rules are more complex than those of many other countries which dictate:

• when and how shares or rights are taxed;

• exemptions and concessions only upon compliance with strict eligibility criteria; and

• reporting and compliance obligations for employers.

McR successfully acted for Mr Davies in Davies v Deputy Commissioner of Taxation [2015] ATC 20-520, which clarified the treatment of contingent rights to acquire shares and gave rise to the proliferation of ‘indeterminate rights’ plans.

GST was introduced on 1 July 2000 with the aim of replacing a number of State taxes (including stamp duty) with a broad based consumption tax collected by the Federal Government and distributed amongst the States and Territories. The proposal and introduction of GST fundamentally changed the collection and distribution of tax in Australia.

While some State taxes were abolished upon the introduction of GST, duty continues to be a significant source of state revenue throughout Australia and in many instances the abolition of some types of duty has coincided with an expansion of duty on land-related transactions and dealings in trusts.

Special Counsel, Jodie Robinson and Senior Associate, Elise Emmerson’s wish for tax reform is to increase GST from 10% and reduce or remove State taxes because GST is a far more efficient tax.

The income tax consolidation regime allows a wholly owned group of related companies to operate as a single economic entity for income tax purposes – filing a single tax return and allowing profits and losses to be offset between group members.

While other countries have group taxation systems, few match Australia’s tax consolidation regime which stands out for integrating group companies into one ‘single’ taxpayer entity.

Despite being introduced under the premise of making group taxation fairer, more efficient, and less costly - the rules are complex and the regime was initially only adopted by the ‘big end of town’.

The use of consolidation remains a key part of our tax structuring and corporate reorganisation work – more and more, the regime is being used by privately owned groups, particularly those looking to restructure, transfer assets between group members, or utilise group losses.

Partner, Melinda Peter's wish for tax reform is a wholesale review of the Australian tax system to meet the changing nature of our economy. Melinda says, "Australia’s tax and transfer system is arguably one of the world’s most complex – which is surely of very little benefit to anyone other than tax advisers! It has long been recognised that an effective taxation system should be based on the premise of achieving fairness, efficiency and simplicity. It is doubtful whether Australia’s current taxation regime achieves any of these criteria. In fact, our current system is arguably the exact opposite - inefficient, technically complex and often distortive. The fact that some of the most complex provisions relate to small and medium sized enterprises – for example, Division 7A, Division 6 and the small business CGT concessions is nonsensical and requires review."

Following the introduction of GST, the States became increasingly reliant on land-based duties, and they were all expanded.

The McR Tax team advise and assist clients to navigate the minefield of potential duty issues which arise in the context of a transaction with even a remote connection to Australian land, assisting fund managers, resource and renewables project operators and foreign investors.

McR successfully acted for Sojitz Coal Resources Pty Ltd against the Commissioner of State Revenue ([2015] QSC 9). McR argued that Sojitz’s acquisition of more than 50% of the shares in Minerva Coal Pty Ltd did not attract duty under Queensland’s former land rich duty provisions because Minerva’s mining leases did not form part of its landholdings. The case has enduring significance in its support for a more limited application of the concept of ‘interests in land’.

Partner, Duncan Bedford’s wish for tax reform is to remove barriers for investment in key industries. He says ‘Queensland’s agricultural sector is missing out on crucial capital investment that could enhance productivity and efficiency due to a land tax system that is deterring potential investors.’

Senior Associate, Caitlin McKenna’s wish for tax reform is to reduce the duty risk of collective investment in property development and infrastructure projects.

Lawyer, Liberty Humphreys’ wish for tax reform is to replace stamp duty with an annual land tax which is levied on unimproved land value, starting with certain property classes such as residential or first-home buyers.

We’ve included McR Tax team’s wishes for tax reform across this time line, and summarise below what we hope to see occur in the future.

My wish for reform is for a simplified tax regime which applies consistently throughout Australia so as to remove the revenue law barriers to investing in Australian assets and people. The abolition of antiquated State taxes such as payroll tax and stamp duty ( even if at the expense of an increase in the GST rate), the reduction in the punitive rates that are charged for Queensland coal royalties and the removal of the duplication of costs caused by having both State and Federal revenue authorities would be a good start.

My wish for tax reform is for the Government to instigate a significant, wholesale review of the Australian tax system to meet the changing nature of our economy. Australia’s tax and transfer system is arguably one of the world’s most complex – which is surely of very little benefit to anyone other than tax advisors! It has long been recognised that an effective taxation system should be based on the premise of achieving fairness, efficiency and simplicity. It is doubtful whether Australia’s current taxation regime achieves any of these criteria. In fact, our current system is arguably the exact opposite - inefficient, technically complex and often distortive. The fact that some of the most complex provisions relate to small and medium sized enterprises – for example, Division 7A, Division 6 and the small business CGT concessions is nonsensical and requires review. On a smaller scale, the removal of payroll tax (which is overly complex, leads to anomalous outcomes and arguably adds nothing other than an additional cost to business (and penalises those larger businesses who are assisting the economy by expanding the Australian workforce) should also be considered.

To remove barriers for investment in key industries. “Queensland’s agricultural sector is missing out on crucial capital investment that could enhance productivity and efficiency due to a land tax system that is deterring potential investors. Current land tax provisions are impacting potential investment from large players like superannuation funds and driving investors across the border into New South Wales.

Consistency and certainty. “The Commission’s approach to statutory interpretation and administration (including audit activity) has not always been transparent and often lacks certainty. On difficult issues (such as unpaid present entitlements, section 100A, and section 99B), the Commissioner’s current approach seems to be to continually seek to evolve and expand the reach of legislation which has been around for fifty years or more. Certainty and consistency are the hallmarks of a fair tax system.”

To introduce tax and duty concessions to facilitate intergenerational transfer of assets.

To increase GST from 10% and reduce or remove state taxes; and to simplify Division 7A to encourage compliance and reduce the costs of compliance.

To see greater legislative or judicial clarity on where payroll tax employment agency provisions will be engaged and how payroll tax is applied to employment agency arrangements.

For the interaction and consequences of CGT rollovers and subsequent consolidation to be amended to ensure both can be used to achieve what is clearly intended; for the small business CGT concessions thresholds to be increased in accordance with CPI, and for the CGT regime to never be expanded to taxing unrealised capital gains.

To see the long overdue modernisation of the Customs Act and the Excise Act, and to rewrite Division 6 of the 1936 Act on the taxation of trusts, so that the law reflects today’s realities.

To reduce the duty risk of collective investment in property development and infrastructure projects. To encourage collective investment in key property development and infrastructure projects, investors’ acquisitions in landholding vehicles should be disaggregated where they are unrelated, acting independently and in their own interests.

To consolidate both the Income Tax Assessment Act 1936 and 1997. This would provide a unified and modernised framework which would enhance clarity, reduce compliance costs, and improve accessibility for all taxpayers.

To optimise the ATO’s response times (and modernise ATO protocols) to reduce taxpayer stress and anxiety when dealing with complex compliance and enforcement matters.

The complexity of Australia’s tax system disproportionately impacts the most vulnerable members of our community; those who are least equipped to navigate it. For people facing financial hardship, language barriers, limited digital access or lower levels of education, understanding and complying with tax obligations can be overwhelming.